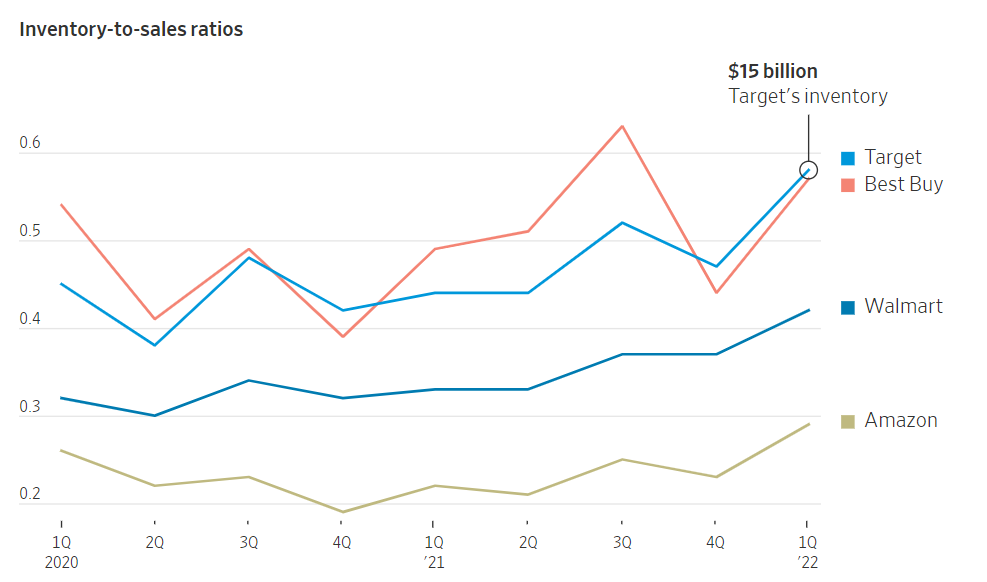

In recent weeks many financial headlines have blared warnings on growing inventory levels across the major US retailers. Since Target and Walmart reported earnings in mid May, sentiment on the sector and the broader economy has become notably concerned about shifting buying patterns and demand from lower-earning households. Management teams at these companies have attributed the growing inventories to their intent to increase SKU availability in reaction to broad shortages seen earlier in the pandemic. Increased freight costs also are represented within the inventory dollar amount carried on the balance sheet, a result of higher ocean-borne shipping rates and higher use of air freight.

Some retailers like Target noted that inventory at the end of Q1 2022 skewed towards quarantine-friendly categories that are no longer seeing strong performance. Target CEO Brian Cornell made the decision to deeply discount home goods, appliances, televisions and casual clothing. This move lowered Target’s full year gross margin, sending operating profit margins down from about 10% to the mid single digits. At their recent annual investor presentation, Walmart US leader John Furner called out that 20% of the inventory they’re now carrying are items they “wish they did not have.” Both Target and Walmart management called out Q2 and Q3 as the timeframe where excess inventory would be discounted.

While DTC companies may have less of a concern about cluttering up physical store spaces with out of season items, it is key to observe what product categories are seeing strength so that adjustments can be made. We dug into the several companies in the Bainbridge DTC index, looking into key product categories at companies that also have at least 3 to 5 years of data. We have focused on inventory as a share of sales and gross margin trends for these brands, and gathered extra detail from the most recent earnings reports to determine the primary drivers.

Note: Graphs Displays Ending Q1 Points in Time Only

The furniture and home goods category is clearly building inventory with Bainbridge DTC index members Lovesac and Purple Innovation showing increases in inventory as a % of sales when compared to pre-pandemic. Lovesac management touted their differentiated product and word of mouth reliant marketing model, and mentioned that their mid and high-end offerings continue to perform well. The company reiterated its guidance even as there was a clear slowdown in their entry level portfolio that caters to lower income customers. Lovesac CEO Shawn Nelson referred to their growing inventory as non-seasonal with a small number of SKUs that sell year round, positioning them well to support a growing customer base. Their margins have been stable, with no intent to increase discounting to meet guidance and no resistance to price increases.

The slowness in home goods is especially impactful to commoditized products like mattresses. Purple Innovation’s inventory jumped to 18% of Q1 2022 annualized sales, more than double any Q1 in the last 5 years. The company struggled in Q1 2022 as sales declined 23% YoY compared against a stimulus-aided Q1 2021. Management reduced full year 2022 sales guidance by 18%, cut headcount, and reduced cost per click advertising. Softness came from deterioration in ecommerce sales (-36% YoY) as Q1 progressed reflecting a “general rationalization” of a quarantine friendly category combined with a shift to in store buying. Management also called out customer resistance to price increases in the quarter. Company gross margin declined in Q1 primarily driven by a large shift toward wholesale and away from eCommerce (67% of mix down to 60%).

Another category that has been challenged is casual wear which many people gravitated towards during the pandemic. This includes athleisure wear, hoodies, jogging pants, and comfort footwear. Lululemon has one of the most pronounced YoY increases in inventory throughout the Bainbridge Index, with inventory jumping 74% YoY while sales grew at a rate of 32%. Lululemon’s CFO mentioned they are focused more on matching their 3YR compounded annual growth rate of sales vs inventory. Q1 20 is elevated for many companies as the March 2020 period was notably weak for discretionary consumer demand. Lululemon has seen one of the most impressive sustained growth stories in 2022, as the company “saw no lift from Q1 2021 stimulus” so sales growth is actually accelerating in 2022. Supporting this growth in store and online will require higher inventory levels (guidance is inventory YoY growth peaks in Q2, and will drop in H2 2022).

Oxford Industries’ Tommy Bahama brand saw extremely strong performance in Q1 2022, demonstrating another sign that branded casual apparel is still performing well. The brand grew 46% YoY, versus the total company rate of 33% (Tommy Bahama is 64% of total Oxford sales). The brand’s very prominent orientation towards vacation and linen wares has boosted its sales in the women's segment, as demand shifts from casual leggings to higher priced occasion dresses. All channels remained in growth mode as eCommerce grew 20% (25% of sales) against retail store sales of 49% (39% of sales). Oxford raised its full year EPS guidance by 11% on improvements in sales and gross margin and has increased their inventory to a 5 year high to support their rapidly improving outlook.

While broad consumer demand remains strong, it is safe to conclude that the lower end of the income spectrum is seeing pressure from rising gas and food prices. Target and Walmart cater to that income segment and obviously have an immense range of products, therefore carrying more risk of abrupt changes in customer buying patterns. As they discount these products, it remains to be seen in Q2 and Q3 how this will affect margins of online DTC players. DTC brands that are least exposed to these inventory buildup trends are those with relatively narrow and differentiated product portfolios, loyal ecommerce customers, and a mix toward upper middle income earners that are not stimulus reliant. Aside from these consumer facing aspects, robust inventory forecasting that takes into account lead times and in transit units is offered within the broad Bainbridge toolset. Book a time now for an intro to all of Bainbridge’s capabilities!